For years, my job was to decide whether a building was worth tens of millions of dollars.

Multifamily real estate. Private equity. Models that said buy this apartment complex, pass on that one, and here is exactly what has to be true for the number to work.

I sat across the table from people who move capital the way most of us move a checking-account balance, and I learned how they actually think.

It is almost nothing like how most people are taught to think about their own money.

Here is the part that took me embarrassingly long to notice: I ran that entire apparatus for other people’s portfolios and rarely pointed it at my own life.

The tools were sitting there.

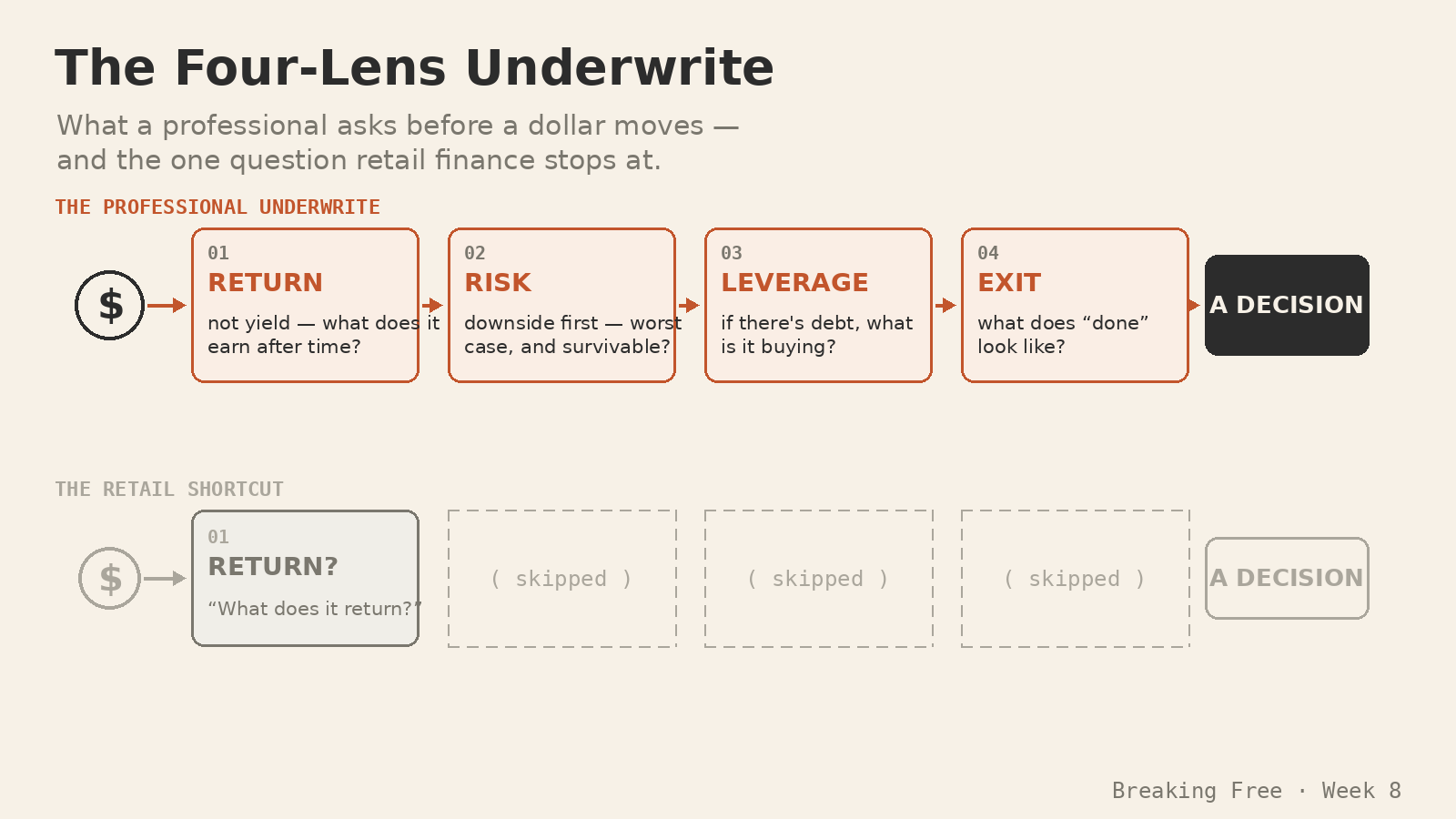

Return. Downside. Leverage. Exit.

Four questions a serious investor asks before a dollar moves, and four questions almost no one asks about their salary, their house, their savings, or their next ten years.

Let me hand you the lens.

What a professional asks before a dollar moves: return, downside, leverage, and exit. Retail finance usually trains you to ask only one question: what does it return?

Yield is not return

Retail finance sells you a number.

The APY on the savings account. The dividend yield. The expected 7 percent.

A private-equity investor barely cares about yield in isolation. They care about total return over a holding period, and, crucially, they price in time explicitly. A dollar in year seven is worth less than a dollar today, so the model has to justify the wait.

Now point that at your life.

The frugal move, the extra hour spent shaving the cost of something, has a yield. But its return has to net out what that hour could have compounded into somewhere else.

The spreadsheet loves a guaranteed 5 percent saved.

It says nothing about the 50 percent you might have built with the same hours aimed at a skill, a second income, or the people in your house.

Yield is what you keep.

Return is what you keep after counting what you gave up to get it.

Most people optimize the first and never calculate the second.

Underwrite the downside first

Amateurs model the upside.

Professionals model the downside first.

Every deal I touched opened with the same ugly question: how do we lose money here?

Vacancy spikes. Rates move. The exit cap expands. The renovation budget slips. The rent growth story does not show up on schedule.

All of that had to be on the table before anyone was allowed to get excited about the return.

The upside is a hope.

The downside is a plan.

Personal finance sells you the opposite order. It leads with returns and treats the downside, the emergency fund, the insurance, the margin of safety, as boring homework for later.

Reverse it.

Your emergency fund is not timid. It is the downside underwrite that lets you take real risk everywhere else.

Freedom is not only the upside you are chasing.

It is the downside you have already handled.

The person who can survive the bad year is the only one who gets to enjoy the good one.

Debt is a tool, not a confession

Personal-finance culture moralizes debt.

Good people pay it off. Debt is a character flaw. The cleanest balance sheet is the most virtuous one.

A private-equity investor hears that and winces, because leverage is neither virtue nor sin.

It is an amplifier.

Aim it at an asset that earns more than the debt costs and it can multiply options. Aim it at a depreciating obligation and it multiplies the hole.

So the question is never simply debt or no debt.

The question is: what is this debt buying?

A mortgage on a place that lets your family keep the right hours and puts the people who matter within reach is a completely different instrument than the financed upgrade you will resent in eight months, even at the same interest rate.

Underwrite your own borrowing the way I underwrote a building: does the thing it buys throw off more life than it costs?

If yes, that debt may be a rational line on your balance sheet.

If no, the zero-percent offer is still expensive.

Every deal has an exit. Does your life?

This is the one that reorganized everything.

No one in private equity buys without knowing how the story ends.

Before a purchase closes, there is an exit thesis: hold five to seven years, force the value up, sell or refinance, here is the target, and here is the trigger.

You do not put millions into something with no idea what done looks like.

It would be malpractice.

And then most of us run our own lives with no exit thesis at all.

We accumulate more income, more house, more retirement balance, more obligation, with no named version of what it is all converting into.

Just more, indefinitely, on autopilot.

The most sophisticated investors I ever met would never allocate a decade of capital to a deal with no exit.

It is the exact thing we do with the one genuinely scarce asset we have: our time.

Mine arrived the way these things usually do: not in a boardroom, but at a kitchen table in front of a calculation four lines long.

Two kids. The cost of full-time care. The tax on the income I would need just to cover it. The question of whether the job was still buying the life we actually wanted, or quietly consuming it.

I will walk through that number in its own post, because it deserves the room.

What matters here is what it exposed: I had a written exit thesis for every asset I had ever underwritten, and not one for the decade of my own life sitting directly in front of me.

That was the moment the whole plan came up for review.

This week: underwrite one decision

Pick one financial thing you are sitting in right now: a purchase you are weighing, a debt, a job, a savings target, a house, a business line, a consulting idea.

Run it through all four:

- Return, not yield: what does this actually earn me after I count what it costs in time?

- Downside first: what is the worst case, and is it survivable?

- Leverage: if there is debt, what is it buying: an asset, an option, or an obligation?

- Exit: what does done look like, and does this move me toward it?

You do not need a financial model.

You need four questions honest enough to change an answer.

The professionals are not smarter than you. They simply refuse to let a dollar move without asking.

Your advisor may not run this for you. They are not in that room, and plenty of them were never taught to think this way either.

But you can bring the lens home.

This is a lens, not personalized financial, investment, tax, or legal advice.

The spreadsheet is useful. The underwrite is better. It asks what the money is actually buying your life.

Friday: the flip side of a career you were good at, and what happens when the identity you built stops fitting the person you are becoming.

Reply and tell me: which of the four — return, downside, leverage, or exit — is the one you have never actually run on your own money?

— Ashleigh